How to choose a payment gateway in South Africa

Summary: This guide outlines key factors for choosing a payment gateway in South Africa. It covers reliability, payment methods, security, and local support.

Payment gateways enable online payments for the growing proportion of South African consumers that are choosing to make everyday purchases online. Any business that intends to accept payments online will need a payment gateway to do so. Choosing the right e-commerce payment gateway partner can have a significant impact on how effective your payments solution can be.

We’ve put together this guide to help e-commerce businesses choose the right payment gateway for their business.

What is a payment gateway?

An e-commerce payment gateway enables businesses to accept and manage online payments. It connects businesses to payment networks and financial institutions that process and settle payments on their behalf.

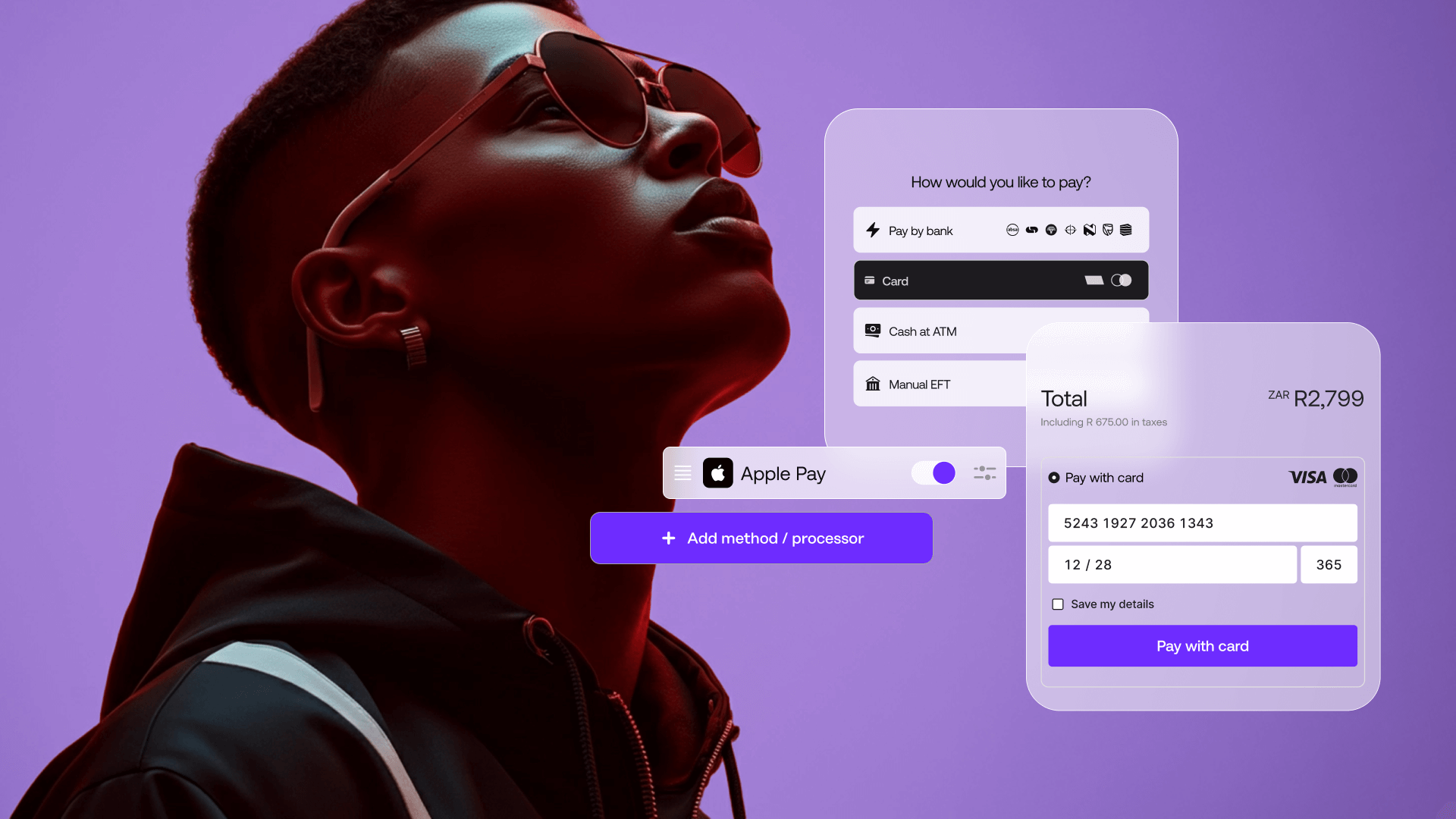

While traditionally focused on card payments, leading payment gateways offer multiple payment methods, which might include:

- Pay by bank or Instant EFT

- Direct bank APIs like Capitec Pay

- Digital wallets such as Apple, Google and Samsung Pay

- Pay with crypto

- DebiCheck or debit order

- Mobile money

- Scan to pay

- And other methods

In addition, payment gateways protect businesses and their customers by protecting sensitive data, like bank account information and card numbers, as well as actively detecting and preventing fraudulent transactions.

How does an e-commerce payment gateway work?

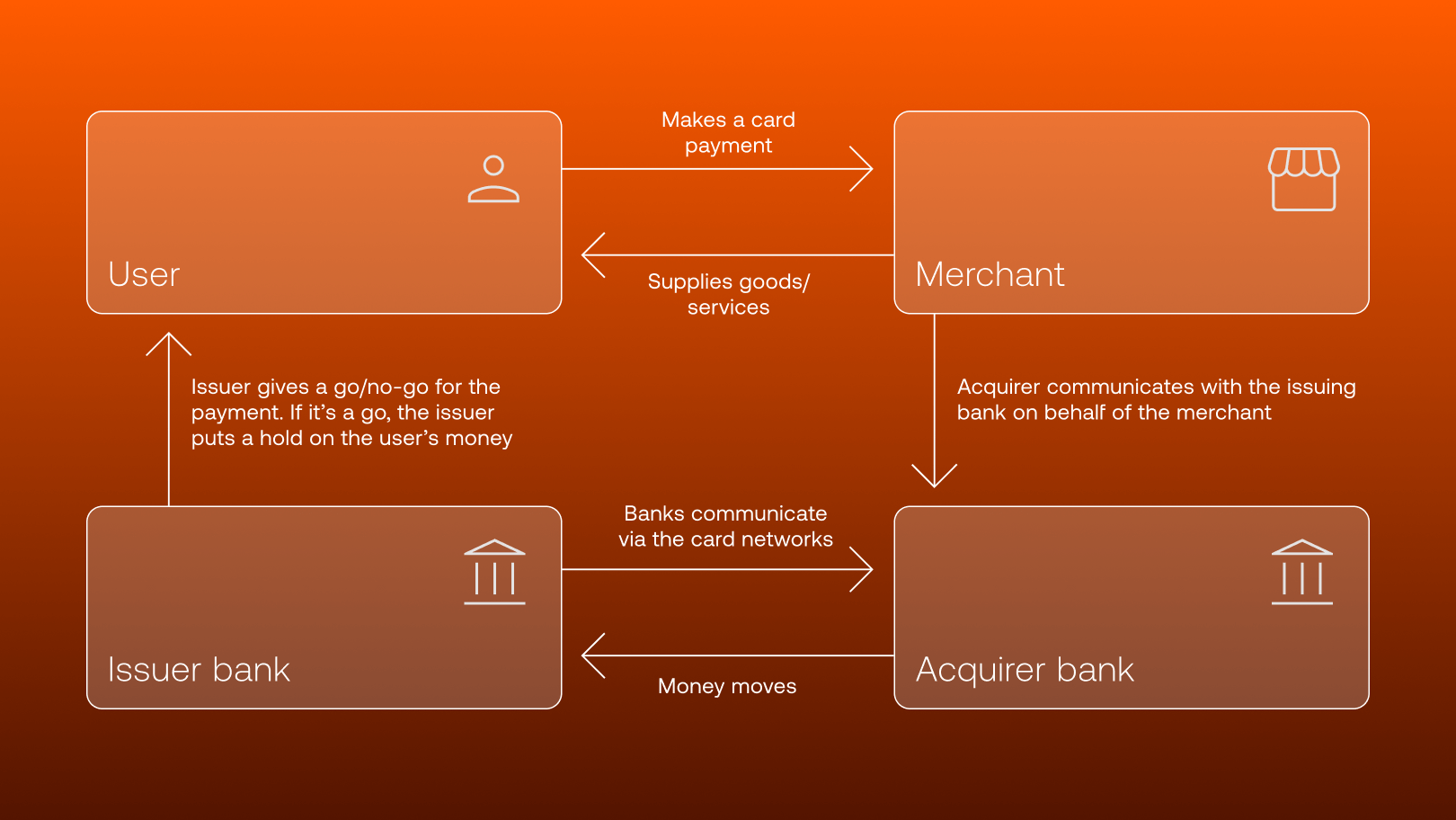

E-commerce payment gateways facilitate the checkout and payment process

A payment gateway manages the end-to-end payment flow once a customer begins the checkout process:

- The customer starts the checkout process.

- The system leads them to a payment page where they select a payment method and enter their payment details.

- Payment details are encrypted and securely transmitted to the customer’s bank for authentication and authorisation.

- Approved transactions are securely transmitted to the payment network and banks to settle the funds.

- A payment confirmation is sent to the customer and the merchant.

Payment gateways vs payment facilitators vs payment processors

The difference between payment gateways, payment facilitators (payfacs) and payment processors is especially relevant for online card payments.

A payment gateway securely transmits payment information and authenticates transactions before they are processed. Payfacs and processors route transactions through card networks and move funds between the issuing and acquiring banks. Both use payment gateways to authenticate online transactions.

The difference between payfacs and processors lies in the acquiring bank relationship. Acquiring banks require merchants to hold a merchant account with an associated merchant ID (MID) in order to settle card transactions. However, not all merchants qualify for or want to manage a merchant account.

Payfacs aggregate multiple businesses under a master merchant account, removing the need for each to have their own master account. It's a great alternative for businesses that aren’t too big to exceed annual card network limits, that are considered to be in a high risk industry or that want to accept card payments quickly.

Payment processors, unlike payfacs, require merchants to hold a direct merchant account with the acquiring bank. They are more suitable for large-scale enterprises that have more complex payment requirements and high volumes. They also act as a processing engine, giving enterprises more control and flexibility through custom-built solutions.

Some payment providers separate their payment gateway solution from their processor or payfac solution. Stitch, however, provides a market-leading payment gateway with each acquiring model, ensuring merchants drive revenue with a robust end-to-end payments engine.

What are the key features to compare when choosing a payment gateway?

A payment gateway’s functionality directly impacts the customer’s checkout experience. The journey needs to be smooth and consistent across all payment methods, and transactions need to be processed at rapid speed and with highest level security. Without these functions, customers abandon the process, and businesses lose money.

- Authentication and authorisation

Before authorising a payment, the payment gateway verifies the payer’s identity. The system uses tools like 3D Secure, biometrics, OTP, CVV verifications and tokenisation to enable early fraud detection. In South Africa, 3D Secure authentication is mandatory for card payments.

Once authenticated, the gateway connects with the payer’s bank to confirm if the account has sufficient funds to complete the transaction.

- Data compliance and security

Global and local data protection standards like PCI DSS and POPIA require merchants to protect sensitive information and use the data only for the intended purpose. To meet these standards, payment gateways use encryption and tokenisation to protect sensitive data such as card and bank account details from data breaches and fraud.

For example, when a customer selects Pay by bank, the gateway directs them to a secure bank login – usually their banking app or browser login – to verify their identity. The log in details should not be stored or managed by the merchant.

PCI DSS-compliant payment gateways like Stitch encrypt card details using robust security protocols. In addition, Stitch replaces card numbers with unique tokens so merchants never store or have access to sensitive data.

- Transaction routing and orchestration

Payment gateways ensure transactions are routed to the appropriate provider, depending on the payment method chosen by the customer. For example, a Capitec Pay transaction is routed to Capitec for processing and settlement.

Advanced gateways optimise success rates with smart routing capabilities. Through payments orchestration, they are able to route transactions to alternative payment processors should the primary one have any issues.

Stitch ensures optimal transaction success and uptime with built-in redundancies and rerouting capabilities. If a particular rail or bank is experiencing issues, Stitch can reroute the payment or offer alternative methods to ensure a higher chance of success.

- Settlement

Payment gateways and processors work together to complete a transaction. Payment gateways ensure approved transactions are processed and confirm that funds have been moved from the customer’s account to the merchant’s account. - Reconciliation and reporting

When a payment is completed, the payment gateway provides details of the transaction to the merchant. These can be accessed through integrated APIs and dashboards that provide real-time transaction data to reconcile with internal and bank records.

Advantages of using an e-commerce payment gateway

Both merchants and their customers benefit from payment gateways in several ways.

Protect revenue and reduce costs

Merchants are in a better position to protect their revenue if payments have been authenticated and authorised. This results in fewer reversals, disputes and chargeback fees.

Smart transaction routing can be used to direct transactions to the preferred payment processor, depending on the payment method. Merchants can prioritise providers with the most competitive commercials and availability to reduce transaction fees and achieve higher success rates.

Improve the customer experience

A payment gateway offers:

- Flexible payment options - Customers have the control and convenience to choose how they pay.

- Trusted payments - Authentication steps build consumer confidence and encourage more online spending.

- Real-time confirmations - Instant feedback on payment success or failure achieves transparency and keeps customers informed.

Access early fraud detection and prevention

Popular and trusted payment gateways use 3D Secure to stop fraudulent payments before they happen. This protects merchants from invalid disputes, chargeback fees and financial loss.

Achieve compliance

Reliable payment gateways in South Africa adhere to PASA, POPIA and PCI DSS regulations. Compliance makes it easier for merchants to operate safely and within legal requirements.

How to choose an e-commerce payment gateway

The right payment gateway ensures a smooth transit of funds, with fast and secure payments. It should also help increase conversion rate and be able to scale with the business as it grows.

What questions should you ask before choosing a payment gateway?

1. Compliance: Does the payment gateway meet local and global standards?

Before anything else, ensure the gateway complies with data security and privacy regulations. Using a non-compliant solution puts your business at risk and could block your ability to accept payments in the future.

Look for these key certifications:

- PCI DSS - the industry standard for handling debit and credit card payments

- ISO 27001 - global benchmark for information security management

Stitch meets the highest possible global data security standards with PCI DSS Level 1 and ISO 27001 certification. Our payment systems are cloud-based and regularly tested with CREST-certified vendors to ensure bulletproof protection.

2. Security: How does the payment gateway detect and prevent fraud?

Like traffic enforcement on a highway, robust security protocols are necessary to protect consumers from bad actors. Popular payment gateways offer OTP, biometrics and 3D Secure to authenticate users before processing payments.

Stitch supports all of the above and goes further by giving merchants greater control to optimise their conversions. Our dynamic 3DS helps merchants tailor authentication to their risk appetite, while seamless token migration gives them ownership of card tokens - making it easy to switch providers without losing saved payment preferences.

3. Payment methods: Does the payment gateway offer the most popular local payment methods?

The right payment gateway should accommodate all of the popular payment methods that are available in the country. The more payment options there are on offer, the more options customers have to complete their orders. However, the merchant should be able to choose the right curated mix of methods that make sense for their customers, to avoid decision paralysis.

For example, digital wallets like Apple Pay, Google and Samsung Pay are becoming increasingly popular among consumers, and are currently in high demand for any online business. Stitch offers a set of SDKs that makes it easy for businesses to integrate all three of these wallets effectively.

4. Speed: How fast can it go and how much can it handle?

Understand the estimated time to market and whether it corresponds with your strategy, and also understand if it can support your volumes - especially if you have high traffic seasons. The highest performance is provided by payment gateways with API-first and cloud-native architecture.

5. Maintenance: How does it stay reliable?

To facilitate payments made at any time and from any location, payment gateways need to be resilient and have nearly flawless uptime (99.9%+).

Additionally, ask the provider about their support structures. Does their system have real-time reporting capabilities and alerts? Do they provide access to local teams for support? How clear are their SLAs, and are they quick enough for you should you run into an issue?

If your team can’t reach them when things go wrong, or if updates cause unexpected disruptions, the cost to your business will outweigh any short term gains.

Stitch offers 24/7, 365 support, led by real engineers who can resolve issues in the moment. They are accessible via any channel, any time there is an issue.

6. Cost: What’s the total cost to use a payment gateway?

Beyond the set up fees, merchants need to understand the day-to-day pricing structure. The approach varies by provider.

Consider:

- Monthly fees, including access, service and maintenance charges.

- Transaction fees per payment method. For example, debit or credit card processing fees would differ from Pay by bank or DebiCheck fees. Depending on the payment method, higher volumes may result in lower fees per transaction.

- Admin fees for disputes and chargebacks and other failed payment costs.

Cost should be weighed against speed, reliability, tech stack, client support, and the overall user experience. A cheaper gateway that’s harder to maintain or scale will cost more in the long run.

Weigh the trade-offs

One size does not fit all. The right fit depends on the business priorities, resources and strategy. Before committing to a solution, understand how the trade-offs can impact the business in the long run. For example, consider:

- Speed to market vs configurability. Plug-and-play setups are quick to deploy but limit the flexibility to customise the checkout experience, authentication settings or reporting. Deep configuration requires more technical integration but ensures the payments stack works well with internal systems and meets unique business requirements.

- Cost vs capabilities. While simpler, cheaper gateways may save on costs in the short term, they may lack the ability to ensure high data security, detect fraud, support an expansive list of payment methods, improve conversion rates and offer support. Responsive incident management and regular system maintenance also can’t be underestimated. While white-glove customer service may come at a cost, it’s essential to ensure the business operates consistently and effectively.

- Local expertise vs global reach. This trade-off depends on the business’ growth plan and target audience. Local gateways ensure that local payment methods are provided to a team of local experts that can advise on changes in the regulatory landscape and they are more accessible to back office teams. International solutions provide access to more currencies but may lack local support.

What to look for — and how Stitch measures up

The criteria this guide outlined aren't abstract. They map directly to real differences between providers, and it's worth being concrete about what meeting them looks like in practice.

- Reliability and uptime: A gateway that goes down during peak trading, such as during Black Friday, month-end or a product launch, costs you revenue and customer trust. The most reliable gateways maintain direct integrations with multiple banks and payment rails, with automatic rerouting to an alternative if one fails. Redundancy at the infrastructure level, not just in policy, is the standard to look for.

- Payment method coverage: South Africa's payments landscape is genuinely diverse. Cards remain important, but Pay by bank options, including Capitec Pay, Absa Pay and Nedbank Direct EFT, are growing rapidly, and digital wallets like Apple Pay and Google Pay are now expected by a significant portion of shoppers. A gateway that supports the full range of South African payment methods through a single integration reduces complexity and ensures you're not losing sales to a missing payment option at checkout.

- Security and compliance: PCI DSS Level 1 is the highest certification available for payment processing. Not all gateways hold it. ISO 27001 certification adds another layer of assurance around information security management. POPIA compliance and adherence to PASA regulations are also non-negotiable for any South African business.

- Integration flexibility: Enterprise businesses typically need to integrate a gateway with existing systems, such as ERPs, CRMs and custom-built platforms. The right gateway offers multiple integration paths: hosted payment pages for faster deployment, embedded form fields for brand continuity and direct API access for full customisation. The ability to keep your own UI and own your network tokens (avoiding lock-in) becomes more important as your payments stack matures.

- Support and escalation: When a payment issue arises such as a bank outage, an unusual spike in declines or a reconciliation discrepancy, the speed and quality of your gateway's response matters. Direct lines of communication, dedicated client success managers and a support team that understands the South African banking environment are worth weighing alongside transaction fees.

- Scalability and orchestration: As transaction volumes grow, the cost of managing multiple payment providers and methods separately compounds. Gateways that offer payment orchestration — a single layer that manages routing, fallbacks and reconciliation across all methods — reduce operational overhead significantly and improve success rates at scale.

Stitch is built around each of these criteria. We hold PCI DSS Level 1 and ISO 27001 certification, maintain direct integrations with South African banks and networks, support the full range of South African payment methods and offers online, in-person and omnichannel payment management through a single platform. Enterprise clients including MTN, Vodacom, Takealot and Bash use Stitch to manage complex, high-volume payment operations. For e-commerce businesses on Shopify, WooCommerce, Squarespace or Webflow, Stitch Express provides access to the same payment infrastructure through a self-serve plugin.

Get in touch with the Stitch team to understand how Stitch can support your payments setup.

FAQs

What should I look for in a payment gateway?

Key considerations include compliance with local and global payment standards, data protection and security protocols, payment method coverage, technology used to support the infrastructure, maintenance and processing costs.

How do payment gateways differ from one another?

Some payment gateways purely function as the approval leg of processing online payments while others include payment processing - the movement of funds - within the solution.

Why does choosing the right payment gateway matter for a business?

The right gateway ensures faster checkouts, better conversion rates, fewer failed transactions and stronger fraud protection. Businesses can benefit from the enhanced customer experience and create opportunities to grow revenue through online storefronts.

The wrong choice, on the other hand, can become a hefty cost. Latency, downtimes, fraud and payment errors deter customers and risk the business’ reputation.

Which payment gateway is best in South Africa?

The best payment gateway depends on your business model, transaction volumes, customer preferences and integration needs. Stitch is widely used by South African enterprises for its flexibility, compliance and robust APIs.

Can I switch gateways easily if I choose the wrong one?

Yes, if that’s the flexibility your current provider gives you. Stitch makes migration easier through features like token migration, allowing you to retain saved payment methods without disrupting customer experience.

How does Stitch compare to other payment gateways for growing businesses?

Stitch offers South Africa’s most reliable payment gateway. Our end-to-end payments engine includes a unified platform with advanced orchestration tools, built in redundancies, dynamic 3DS and advanced data protection to build and scale online payments. We ensure enterprise businesses grow revenue with intelligent payment solutions and white-glove support.

What is the best payment gateway for enterprise businesses in South Africa?

The best enterprise payment gateway depends on your business's specific requirements, including transaction volumes, payment methods needed, integration complexity and support expectations. For enterprise businesses in South Africa, the most important criteria are reliability (direct bank integrations with automatic fallback), breadth of payment method coverage (cards, Pay by bank, digital wallets, debit orders), PCI DSS Level 1 certification, and the availability of payment orchestration for managing multiple methods and providers at scale. Stitch is widely used by South African enterprise businesses for complex payment operations, including companies such as MTN, Vodacom, Takealot and Bash.

What should I look for in a payment gateway in South Africa?

Key criteria include: PCI DSS Level 1 and ISO 27001 certification; support for all South African payment methods including cards, Capitec Pay, Pay by bank, Apple Pay, Google Pay and debit orders; reliable uptime with multi-bank redundancy; flexible integration options (hosted pages, embedded fields or direct API); transparent reporting and reconciliation; POPIA compliance; and a support model suited to your business size. For enterprise businesses, payment orchestration capabilities and dedicated client support are also important. For smaller e-commerce businesses, ease of setup, plugin availability for Shopify or WooCommerce, and self-serve onboarding are the priority.

What is PCI DSS and why does it matter when choosing a payment gateway?

PCI DSS (Payment Card Industry Data Security Standard) is a set of security standards created by Visa, Mastercard and other card schemes to protect cardholder data. PCI DSS Level 1 is the highest certification level, applying to organisations that process over six million card transactions per year. When a payment gateway holds PCI DSS Level 1 certification, it means its systems have undergone rigorous independent security testing and meet the most stringent global standards for handling card data. For merchants, using a PCI DSS Level 1 certified gateway simplifies your own compliance obligations — particularly if you use hosted payment pages, where the gateway takes on the majority of PCI scope.

What is the difference between a payment gateway and a payment processor?

A payment gateway is the technology that captures and transmits payment data from a customer to the relevant financial networks — it handles the front-end of a transaction, including authentication, fraud checks and routing. A payment processor handles the actual movement of funds between banks once the transaction has been authorised. Some providers offer both gateway and processing services in a single integration, which simplifies operations and can improve success rates by eliminating the handoff between separate systems. Stitch offers end-to-end payment infrastructure covering both gateway and processing capabilities, including card acquiring through Efficacy Payments.

Can I switch payment gateways without disrupting my customers' saved payment methods?

Yes, in most cases. If you have returning customers with saved card details or linked bank accounts, token migration allows those stored payment credentials to be transferred to a new gateway without customers needing to re-enter their details. This is an important consideration when evaluating a switch: ask any prospective gateway provider whether they support token migration from your current provider before committing.