Lay-by vs Buy Now Pay Later: what's the difference?

Lay-by requires customers to pay before they receive the goods. BNPL lets customers take the goods immediately and pay later, over time. This article explains the key differences, the risk profile for merchants and which model is better suited to modern e-commerce.

Both lay-by and Buy Now Pay Later (BNPL) allow customers to spread the cost of a purchase across multiple payments. But they are fundamentally different models with very different implications for conversion, cash flow and operational complexity.

Understanding the distinction matters for South African merchants deciding how to address affordability at checkout, particularly as BNPL has become a live option in the local market.

How lay-by works

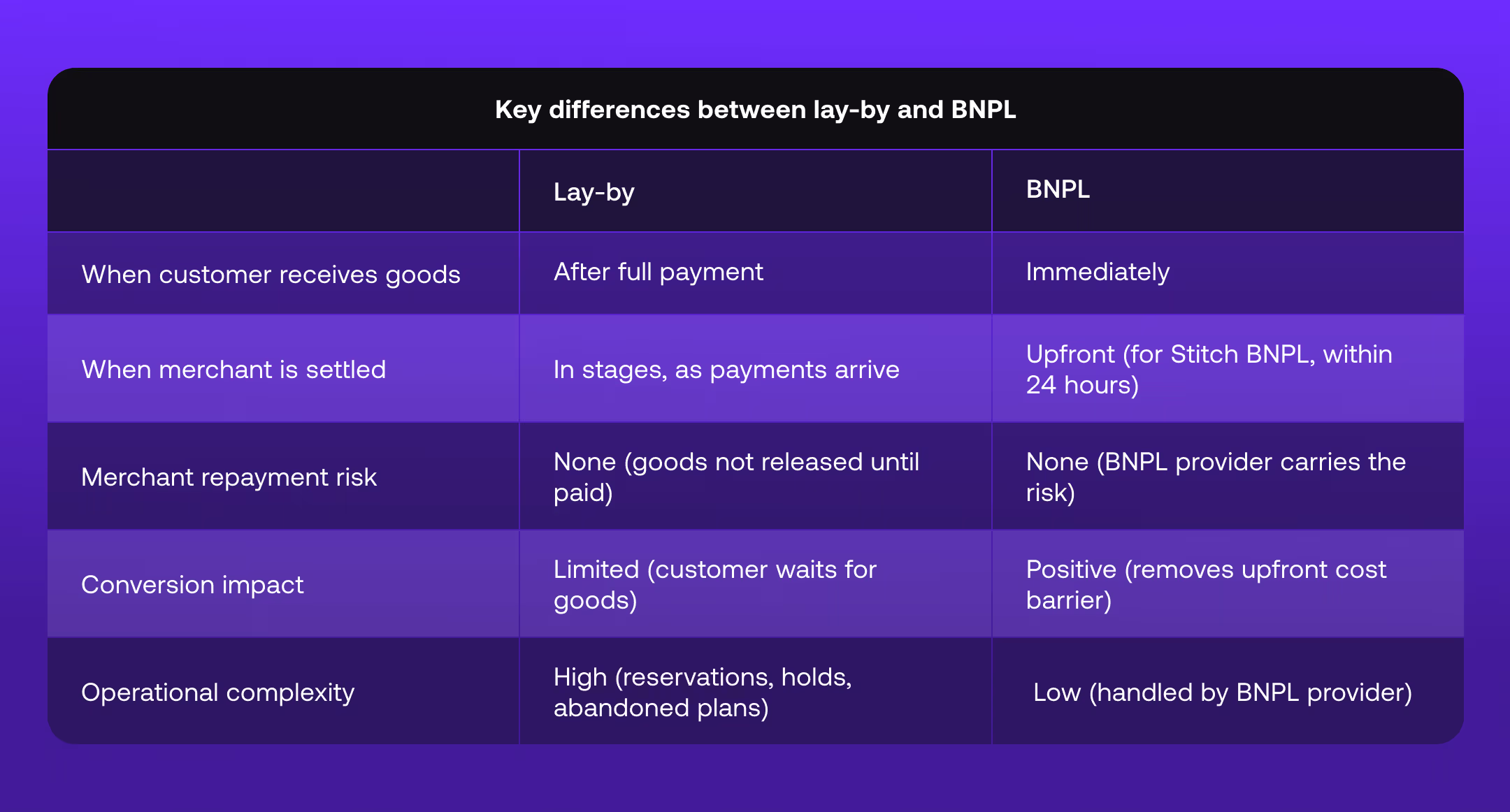

Lay-by is a deferred fulfilment model. The customer makes a series of payments toward the total purchase price, but does not receive the goods until the full amount has been paid. The merchant holds the item while the customer settles the balance over a defined period, usually weeks or months, depending on the agreement.

From the merchant's perspective, lay-by is low-risk: they do not part with the goods until payment is complete. From the customer's perspective, the core limitation is that they cannot use the product while they are paying for it. For items driven by immediacy such as clothing, electronics, event tickets, this friction significantly reduces the appeal of lay-by compared to alternatives.

Lay-by also requires merchants to manage reservation systems, inventory holds and communication flows with customers over an extended period. The operational overhead is non-trivial, and abandoned lay-by plans, where customers stop making payments before completion, create additional complexity around refunds, restocking and customer relations.

How BNPL works

BNPL is a deferred payment model. The customer receives the goods immediately and pays the purchase price in instalments over time, typically across three, four or six payments. Crucially, the merchant is settled in full upfront. With Stitch BNPL, settlement happens within 24 hours. The BNPL provider then manages the customer instalment relationship on behalf of the merchant and carries any repayment risk.

This is the structural distinction that makes BNPL significantly more attractive for e-commerce: the merchant's cash position is identical to a normal sale, but the customer gets the affordability benefit of spreading the cost. Neither party is disadvantaged.

For customers, the immediacy matters enormously. Research consistently shows that purchase intent decays quickly. The longer the gap between decision and possession, the more likely the customer is to abandon the purchase or find an alternative. BNPL captures the sale at the moment of intent.

Key differences between lay-by and BNPL

Who benefits from lay-by in the South African context?

Lay-by retains relevance for specific segments of the South African market, particularly lower-income shoppers who do not qualify for credit products and for whom the delayed fulfilment is an acceptable trade-off for affordability. For some product categories, particularly large furniture or appliances, the lay-by model has genuine utility.

However, lay-by is not a checkout conversion tool. It does not capture impulsive or time-sensitive purchases, and the operational overhead is a meaningful cost for merchants.

Why BNPL is better suited to modern e-commerce

For e-commerce businesses targeting the growth segment of digitally confident South African shoppers, which are mid-to-high income earners making considered purchases online, BNPL is the stronger model.

According to Stitch’s upcoming 2026 consumer payments report, 71% of credit-active consumers use BNPL at some frequency, and BNPL adoption is highest among mid-to-high income earners using the service for larger purchases. This results in meaningfully higher average cart values for merchants that offer it. The customer takes the goods immediately; the merchant is settled in full. Neither party carries inventory risk or repayment risk.

BNPL also integrates naturally into a multi-method checkout. It can be presented as a primary option alongside card, pay by bank and digital wallets, or configured to surface only for specific transaction values or categories. This flexibility is something lay-by, as a fulfilment model rather than a payment method, cannot replicate.

Stitch BNPL is now available to South African merchants through the Stitch online payments platform.

What is the main difference between lay-by and BNPL?

With lay-by, the customer pays first and receives the goods only after completing all payments. With BNPL, the customer receives the goods immediately and pays in instalments over time. Merchants are settled in full upfront with BNPL — with Stitch, this happens within 24 hours.

Does BNPL carry risk for the merchant?

No. In a BNPL arrangement through Stitch, the merchant is settled in full immediately. The BNPL provider manages the customer instalment relationship and carries any repayment risk. The merchant's cash position is the same as a regular sale.

Is lay-by still relevant in South Africa?

Lay-by retains relevance for specific segments, particularly lower-income shoppers who do not qualify for credit products and for whom delayed fulfilment is acceptable. However, it is not suited to driving e-commerce conversion, and the operational overhead is significant for merchants.

Which customers use BNPL in South Africa?

According to the Stitch 2025 Consumer Payments Report, BNPL adoption in South Africa is highest among mid-to-high income earners, who use it primarily for higher-value purchases. This results in significantly higher average cart values for merchants offering the method.

Offer your customers flexibility with Stitch BNPL