Behind the rise of Apple, Google and Samsung Pay in South Africa

Summary:This article explores the growth of digital wallets in South Africa. It explains what’s driving adoption and how wallets are changing consumer payments.

Adoption of digital wallets such as Apple, Google and Samsung Pay has increased exponentially in South Africa. Our latest Consumer Payments Report shows that more than 70% of consumers have used digital wallets for daily payments. This is a significant jump from last year’s survey, where 46% indicated they had still never used Apple Pay, Google Pay or Samsung Pay.

As access starts to pick up for online payments using Apple, Google and Samsung Pay, we’re seeing growing interest - and it’s not just hype. Where these methods have launched for online payments, we’re seeing instant and significant adoption.

South Africa is fertile ground for Apple, Google and Samsung Pay

South Africa’s mobile and bank penetration rates have created the ideal environment for digital wallet adoption. According to the 2022 national census, over 92% of households have a mobile phone, and over 60% access the internet through their mobile devices. At the same time, over 85% have access to a bank account.

However, it’s important to note the distinction between contactless payments, which is more widely available in South Africa today, and digital wallet payments which is growing in accessibility.

Digital wallets vs contactless card payments

Digital wallets and contactless card payments both use near-field communication (NFC) technology, but they are not the same. Most notably, contactless card payments are only possible in-person, whereas digital wallets can be used to make payments online and in store.

Contactless card payments use a physical card to complete a transaction. The payment method is “contactless” because it uses NFC to allow customers to tap and pay at point-of-sale (POS), without the need to swipe or insert their physical cards. Depending on the tap-only setting of the card or on their mobile device, a PIN may be required to authenticate the transaction.

On the other hand, digital wallets are app or device-based. The user enters their physical card credentials in the app, which then tokenises the data to save and protect sensitive information. The device authenticates transactions using biometrics. In addition, digital wallets offer expanded payment options, such as making in-app purchases – and enable users to add multiple different cards or payment methods, any of which can be used for an individual transaction.

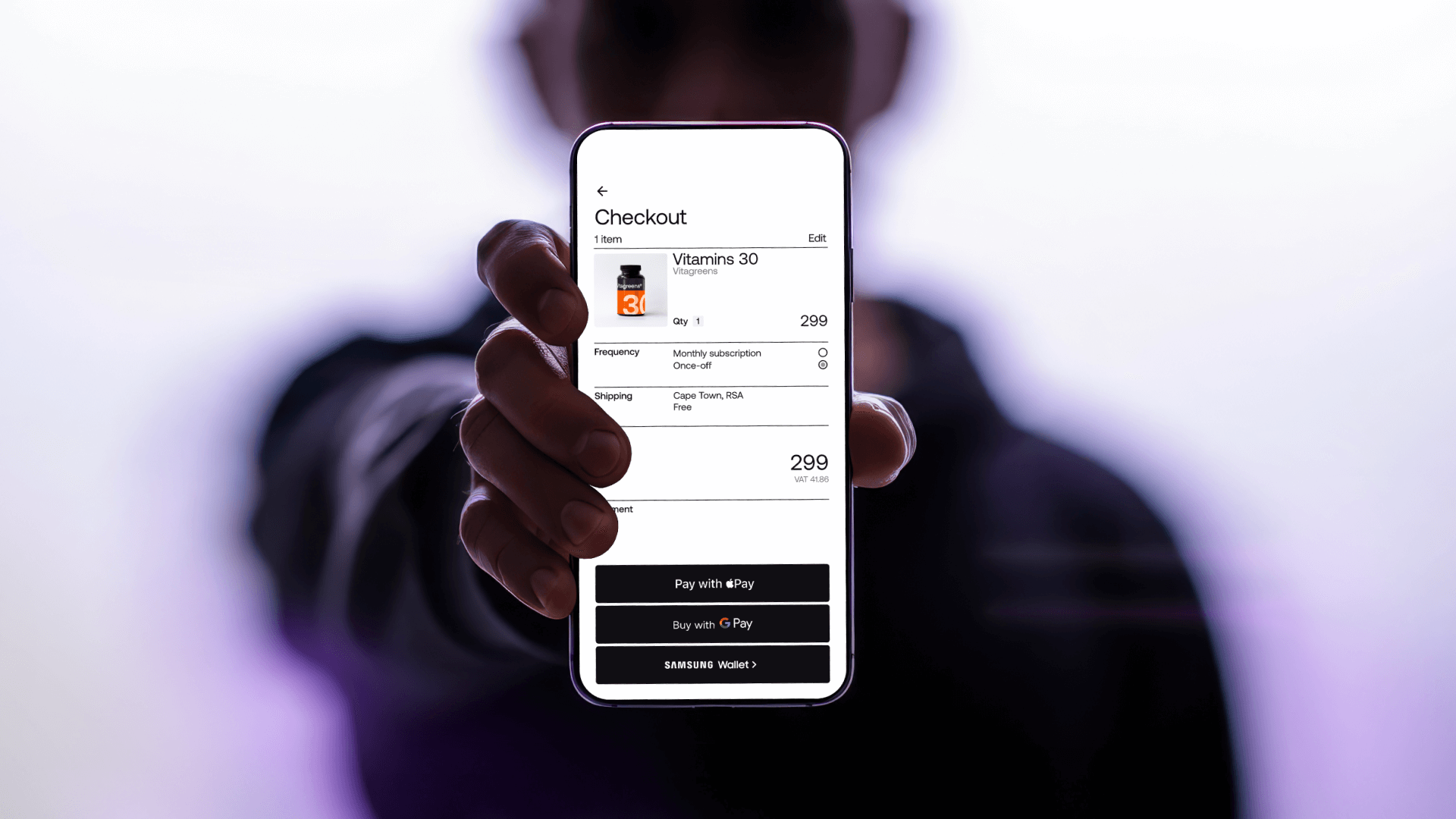

How digital wallets work for online payments:

- Wallet integration: On a merchant’s checkout page, the user selects their preferred digital wallet option (Apple Pay, Google Pay, Samsung Pay). This may also be automatically surfaced depending on the device being used, through PSPs like Stitch.

- Tokenised credential submission: After selecting a card saved in the wallet and authenticating it, the tokenised payment information and a dynamic cryptogram (a one-time-use security code) are sent to the merchant or a payment service provider (PSP) like Stitch.

- Transaction flow: The PSP transmits the data to the card network (Visa, Mastercard), which then routes it to the issuing bank.

- Authorisation: The issuer verifies the token, the cryptogram and the available funds before authorising or declining the transaction.

Digital wallets speed up checkout by removing the need to input card data or complete a 3DS authentication flow. The tokenisation and device-based authentication strengthen fraud protection compared to contactless card payments. Merchants also experience lower interchange fees, reduced chargebacks and fewer disputes, while consumers get to use an app that is free and doesn’t require an internet connection to complete a transaction.

Why adoption of digital wallets is rising in South Africa

Adoption of digital wallets in South Africa is growing steadily. FNB, for example, reports that their digital wallet volumes have increased by 74% between 2023 and 2024.

Why the significant uptake? Digital wallets meet both the needs of the customer and the merchant, and their mobile-first design is a big part of what makes them so appealing.

Convenient, mobile-first design

As more affordable NFC-enabled smartphones enter the market, mobile wallets have become easier to access. Apple Pay, Google Pay and Samsung Pay are popular digital wallets that use device biometrics, NFC and tokenised card credentials to complete payments through a smartphone.

The mobile-first design removes the friction of carrying a physical card and remembering PINs. For online payments, consumers do not have to enter card credentials or complete 3DS authentication to make a payment using their digital wallet, but they receive the same security benefits as if they had used 3DS. As a result of the simplified yet secure payment flow, digital payments are more convenient and conversion rates are improved.

Revenue protection and accessibility

Because digital wallet payments are authenticated, merchants benefit from lower interchange fees, reduced chargebacks and fewer disputes, protecting the merchant’s revenue.

For consumers, the apps are free and don't need internet connectivity to complete a payment. To further boost adoption, some banks offer rewards to cardholders who use digital wallets.

Enhanced fraud protection and security

Card-not-present (CNP) transactions accounted for 68% of total card fraud losses in 2023. While card authentication processes like CVV and 3DS authentication provide strong protection, they can also lead to abandoned carts due to extra verification steps.

Digital wallets use tokenisation and device authentication to deliver strong security and give customers more flexibility to authenticate themselves with biometrics or device PINs.

Increased conversion rates

As mentioned, digital wallets streamline and speed up the payment process, making it easier for consumers to complete their purchases. Some, like Apple Pay, also offer one-click e-commerce checkout, with prefilled addresses.

Our report shows that Apple Pay conversion rates are 42% higher than standard card payments. Within one week, over 33% of iOS users who made purchases used Apple Pay upon launching the method on a major e-commerce site. One likely reason for this is its processing speed - 50% of Apple Pay transactions are completed in under 3 seconds from initiation and 95% under 5.2 seconds.

One in five South Africans are regular digital wallet users

23% of respondents indicated they use digital wallets frequently or always. This presents a clear opportunity for enterprises: by accepting digital wallet payments, you give consumers more control over how they pay - and boost your sales and revenue.

Read our full report.

FAQs

Why are digital wallets growing in South Africa?

Increased smartphone usage, contactless payments, and demand for faster, more convenient checkout experiences are driving digital wallet adoption in South Africa.

How do Apple Pay, Google Pay, and Samsung Pay work?

These wallets securely store card details using tokenisation and allow users to pay via mobile devices using biometric or PIN authentication.

Are digital wallets secure for consumers?

Yes. Digital wallets use encryption, tokenisation, and device-level security to protect payment information and reduce fraud risk.

Where can consumers use digital wallets in South Africa?

Digital wallets can be used for in-store contactless payments, online purchases, and in-app transactions at supported merchants.

How do digital wallets impact businesses?

Businesses benefit from faster checkouts, higher conversion rates, reduced fraud, and improved customer satisfaction when accepting wallet payments.

Will digital wallets continue to grow in South Africa?

Yes. As infrastructure improves and consumer trust increases, digital wallets are expected to play a larger role in South Africa’s payment ecosystem.

Add digital wallets to your payment flows